Five Genuinely Useful Things Crypto Can Do In 2021

Five Genuinely Useful Things Crypto Can Do In 2021

Many people are of the mindset that crypto is only useful for financial speculation. While that was certainly true during the ICO mania of 2017, is it still true today? I spent the past two months tinkering with blockchain based protocols to see if the technology has matured in the past four years. It truly has—blockchain based apps can actually do useful things for normal people.

Here are five things crypto can do in 2021 that it couldn’t do four years ago:

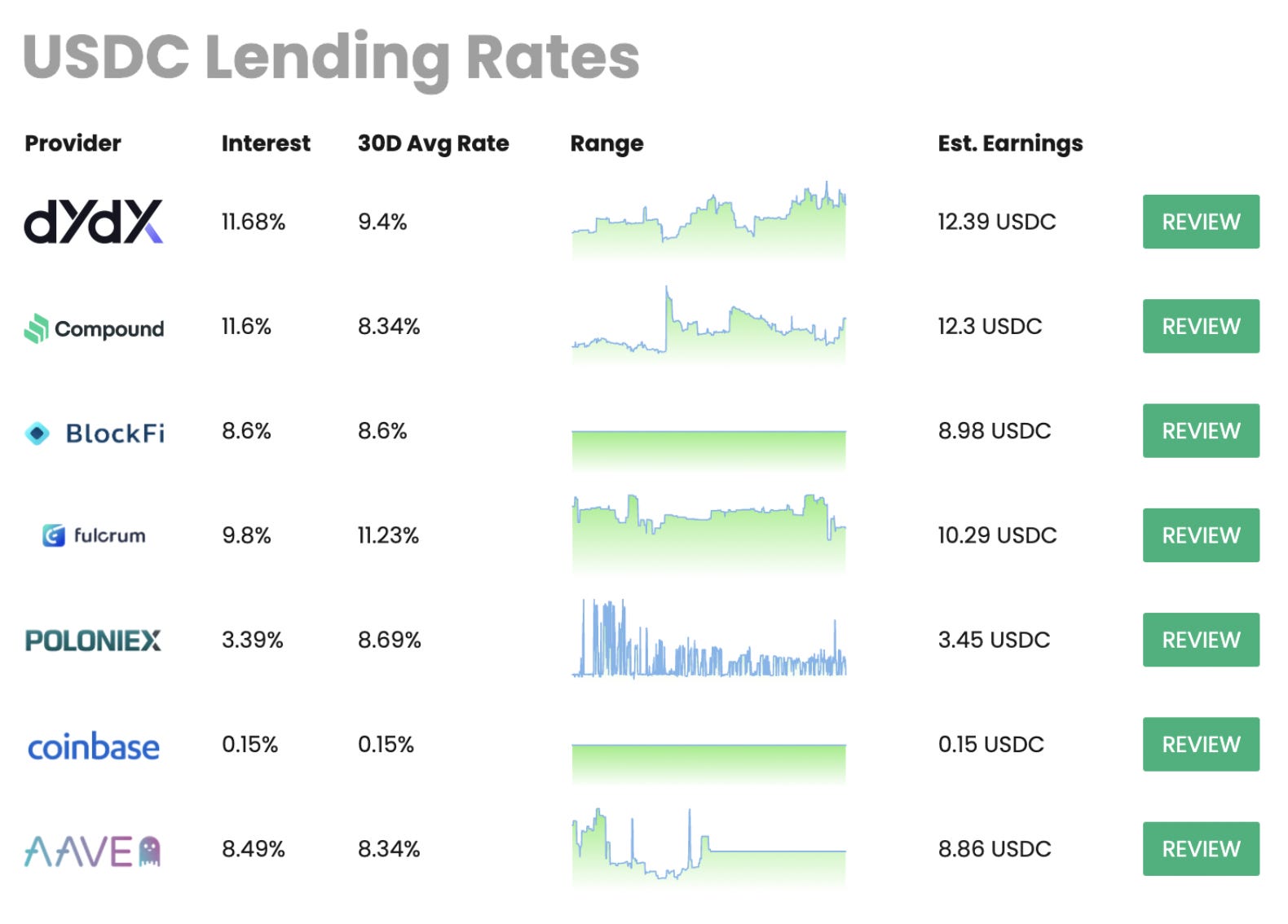

Earn 10% interest on a cash deposit

Take out a crypto backed loan

Send money as easily as Email

Buy stocks and ETFs from other countries

Make and sell digital art

Earn 10% interest on a cash deposit

With interest rates close to zero, money deposited into traditional savings accounts lose value relative to inflation.

In contrast, crypto lending platforms currently offer ~10% APY on deposits. Deposits can be in a number of cryptocurrencies, but stablecoins—coins pegged to the US dollar—tend to earn the highest interest today. Traders use stablecoins in a variety of ways and are willing to pay up to borrow them.

What’s attractive about this use case is that the user does not need to mess with bitcoin or ethereum. All that’s needed is to convert US dollars to a stablecoin like USDC, deposit the USDC into a crypto lending platform and immediately accrue interest.

Crypto lending accounts differ from bank term deposits in two ways. First, there is no fixed interest rate. The APY on stablecoins has fluctuated from 2% to 20% in the past year. Second, there is no term limit. Deposits can be made and withdrawn at any time without penalty less standard transaction fees.

How safe are these deposits? Certainly it’s not comparable to federally insured bank deposits. Crypto lending carries unique risks. If the smart contract governing the deposit has bugs, funds may be stolen. If the governance of the protocol is poorly designed, hostile actors may take over the platform and redirect the funds. These projects are also very young—some merely months old. There are many unknown risks.

Despite these drawbacks, at least crypto is putting something on the menu. Without crypto-lending, professional investors might seek out junk bonds, dividend stocks, or emerging market opportunities—each of which carries risks no less daunting. But for the retail investor, there are no realistic alternatives. Crypto-lending provides an outlet for intrepid individuals to earn some yield.

See also: Where crypto yields come from

Get a Crypto Backed Loan

Let’s say you’ve held some crypto through the last few years and you now need some cash. Perhaps need to pay for a medical expense or start a business. What do you do?

A few years ago, your only option was to sell your crypto. This has two drawbacks. First, this may incur a large tax bill. Second, if crypto truly takes off in the coming years, this might become the worst financial decision of your life.

In 2021, you can take out a loan against your crypto holdings. If you have $100k in ethereum, you can take out a $40k loan at 5.5% APY using MakerDAO in less than five minutes.

These loans are unique in a number of ways. First, they are fully collateralized using your existing crypto assets. As such, the lender does not need to assess your credit worthiness. You can take out a loan without providing any personal information—not even an email. If you fail to meet your obligations, the lender liquidates your collateral.

Second, the interest rate or “stability fee” is variable. For Maker this has been known to vary from 0.5% to 20% depending on the state of the crypto market.

Third, if your collateral falls below a certain threshold (150% of the loan value in the above example), this may trigger a liquidation event. When this occurs your collateral is sold, a 12% liquidation penalty is charged, and the rest of the funds are returned to you. All of this is governed by smart contracts running on the blockchain with no humans in the loop.

Crypto loans are useful for those who already own crypto assets. It doesn’t help people who need a car for their first job. But it’s no different than taking out a loan against your house or taking out margin in a brokerage account. It makes your existing assets more liquid and useful.

Send Money as Easily as Email

Sending money is the original killer use case for crypto, but it has one major drawback: the crypto address looks like gibberish. Email addresses look like: “james@mail.com” while crypto addresses look like: “0x3Cc52a6E7238cd13ab34dc86B7B18d2a8778DA1Z”. Crypto addresses are unreadable, unrememberable, and frankly terrifying. This has held back mainstream adoption of crypto for money transfers.

Ethereum Name Service (ENS) makes crypto addresses human readable. Just as DNS converts internet IP addresses into web addresses, ENS converts 64 character crypto addresses to readable addresses ending with “.eth”.

Let’s say you’re Bryan Smith. You are a content creator with a global following. How do you receive money? You could have a Patreon, but that’s only for recurring payments. You could include your PayPal for tipping. But PayPal is not a global standard. Unlike universal protocols like email, payment apps are fragmented by geography. In the US people use PayPal, Venmo, and Square Cash. In China it’s AliPay and WeChat Pay. In Latin America it’s Samsung Pay and Mercado Pago. Almost none of these services are interoperable.

Just as you can register bryan.smith@mail.com and get on one universal email standard, you can register bryansmith.eth and get on one universal internet money standard. By including bryansmith.eth on his website and business card, you can receive bitcoin, ethereum, and other crypto currencies from anyone in the world. A transfer costs less than $1 using Litecoin and settles in minutes.

ENS makes crypto addresses memorable and readable. It makes internet money transmission as universal and dependable as email.

Buy Stocks and ETFs From Other Countries

Most people can only buy stocks listed in their own country. Those who have the good fortune to own US equities, especially in technology, have done very well in the past decade. But just 4% of the world’s population live in the United States. If the birth lottery placed you in Croatia, Mali, or Thailand, your chances of owning Amazon or Tesla are slim to none. The lack of access cuts both ways. A hot tech IPO on India’s NSE exchange is likewise out of reach for most American investors.

Stocks are digital bits, but because they live on traditional financial rails, they are siloed by country. Converting them to true “internet bits” would make them globally accessible.

Mirror protocol has now done just that. Mirror creates synthetic assets that track the performance of their real world counterparts. Users can buy “mTSLA'' tokens to get exposure to Tesla or “mSPY” tokens to track the S&P 500 and so on. These mirror assets do now grant ownership of the underlying, they only reflect price movements. Mirror is popular in countries such as Thailand, Malaysia, and South Korea. It currently facilities ~$20 million in daily trading volume.

As is the norm in crypto—people can use Mirror without supplying credentials, filling out forms, or going through intermediaries. It is permissionless to use.

By moving regional assets onto international blockchains, Mirror extends financial inclusion.

Make and Sell Digital Art

Despite the countless articles written about Non-Fungible Tokens (NFTs), people still find them perplexing.

To understand NFTs, pretend for a moment that you’re an artist—a well regarded photographer.

Each year you release 12 new pictures. Each picture is released as 50 prints. Each print is priced at $500. Each year you earn 12 x 50 x $500 = $300,000 in gross income.

You have a website for taking orders. But other than that, the business is entirely analogue. You print photos, pack them, and ship them to clients.

Your camera is digital. Your workflow is digital. Your clients would prefer to buy digital. Why can’t you sell them digital files?

Because there’s no way to create a file that only has 50 copies. Computer files can be copied infinite times. And no one pays for something that has infinite copies.

NFTs make it possible to create a finite number of digital items on the internet—it enables digital scarcity. Each NFT has a unique cryptographic signature. While the artwork can be copied, the signature can’t, thus ensuring a finite number of authentic “prints”.

Prior to the invention of NFTs, you as an artist can only make a living by shipping physical packages to your clients each month. Using NFTs, you can replicate your entire photography business with digital files and signatures. Each month, instead of printing 50 images, you mint 50 NFTs. You sell the NFTs online for $500 each. You generate $300k of income with purely digital art. As an added bonus, NFTs automatically track secondary sales of your artwork. If your clients re-sell the artwork, 10% of the proceeds go to you.

From a non-existent category four years ago, NFTs now generate over $200 million of sales a month.

Final Thoughts

Crypto used to be the premier asset for financial speculation. It still is, but it now can do so much more. The use cases of savings, borrowing, and sending money is relevant to billions of people worldwide. Being able to create, sell, and purchase scarce digital goods creates jobs and adds new value to the economy.

Crypto proponents have always argued that speculation would eventually lead to utility. I think we are finally there.

as a normal person, I shall say i finally could relate those fancy terms with my daily application. Thank you.

And why don't you better get 20% fixed apy on UST stable coin with Anchor Protocol on Terra? No brainer.